Low rates. How long will it last?

BY LISA SCONTRAS

BY LISA SCONTRAS

CUSTOM PUBLISHING GROUP

Fifty years ago,a loaf of bread cost 20 cents,a gallon of gas 25 cents,a new car a whopping $2,600,and a new home could be scooped up for less than $20,000. Television was in black and white and no one had ever heard of a desktop computer. For the most part,life today is quite different and the cost of living is exorbitantly higher,except for one thing: Interest rates.Right now, mortgage rates are still grooving at 1960s levels.

According to Freddie Mac’s weekly survey of conforming mortgage rates, the 30-year fixed-rate mortgage averaged 4.72 percent,down from last week’s rate of 4.79,and 5.59 a year ago.While mortgage interest rates have been hovering in the sub-5 percent range on and off for a few months,Carl Worthy,director of training at Prudential Locations,says,”Many people forget how we got here and don’t realize that these low rates are temporary,not a new norm.”The Federal Reserve intervened in late 2008 to purposely reduce long-term interest rates,”he continues. “It worked.

At one point just after the intervention began,rates slid below 4.25 percent. We are not likely to ever see rates go that low again.”When the federal intervention ended in March,rates climbed briefly and then retreated.Worthy explained why rates have recently dropped back. “World events like Europe’s current credit problems in Portugal,Italy,Ireland,Greece and Spain,have created an increased demand for U.S.10-year Treasury Bonds,”he says. “This surge in demand has increased the purchase price of the bonds,and thereby has reduced the yield the bonds provide.

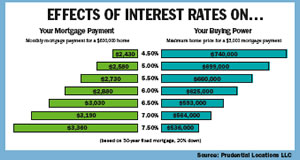

Since long-term interest rates,like home mortgage rates,are tied to the return on these bonds, the lower return has reduced mortgage interest rates again … temporarily.” So for now, there is a plateau,and perhaps one last chance for home buyers to lock in the rate of a lifetime. What does this mean to you? Here are three significant advantages: 1. Lower monthly payments.The lower the interest rate,the lower the monthly mortgage payment. “For example,a point and a half drop in interest rate is the same as a 15-percent reduction in purchase price,” says Worthy,who points out that rates were near 6.5 percent before the Feds intervened.Now,they’re just below 5 percent.”A $400,000 home at 6.5 percent costs about $2,025 per month – based on a 30-year loan with 20 percent down – but that same home at 5 percent interest costs only $1,717 per month,”says Worthy.

“This is the same as the seller giving the buyer a 15 percent discount on the home.” 2. Buy more house for the same amount of money. Let’s say the buyer is OK with the $2,025 monthly payment from the first example. If rates were to come down to 5 percent,which is what they are today,instead of buying a $400,000 home at 6.5 percent,the same buyer could bump up their purchase price to $480,000. That’s a significant increase. 3. Qualify for a home when you might not have before.”The third benefit of low interest rates is that more buyers can qualify for loans than ever before,”says Worthy. “There are many buyers who at 6.5 percent or even 6 percent,can’t qualify for a home. But at 5 percent,they can.Just remember,these rates are temporary and could move up again at any time.”Worthy’s advice to renters who really want to buy a home is to “buy whatever you can afford, when you can.” He has made it his goal to get young renters into their first home. “Nothing builds wealth like real estate,and with interest rates this low,it has never been a better time to get out of the rental trap,”he says.

He recommends renters look into the tax benefits of owning a home by taking a copy of their 2009 tax return to a tax preparer or a CPA. Ask them to estimate how much money could have been saved in taxes by owning a property in 2009 with a $300,000 to $400,000 mortgage. Ultimately,tax deductions will put more money into your pocket to help pay a mortgage,he says. “Ask your aunties,uncles and parents … no one regrets the property they bought,”Worthy says.”They only regret the properties they did not buy.”

See More Listings