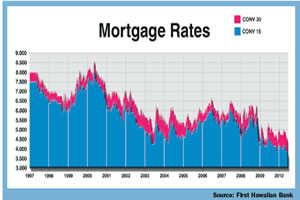

Mortgage Rates Reach Record Low

With mortgage interest rates at a historically low level, prospective buyers who have been waiting for just the right time to make their move are seriously shopping for available properties that meet their needs and fit their budget.

With mortgage interest rates at a historically low level, prospective buyers who have been waiting for just the right time to make their move are seriously shopping for available properties that meet their needs and fit their budget.

Not only are mortgage interest rates at an all-time historic low, there are also good values on the market in various price ranges.With inventory comparatively low, competition for the best buys is heating up…so timing is critical.

So, the big question is, at what point can I “lock in” and, hopefully, take advantage of the rates at their lowest ebb. Provided all documentation is in order, how long should it take to close?

Wesley Young, Senior Vice President of First Hawaiian Bank’s Residential Real Estate Division, notes that just as every borrower’s case is different, so are the policies and procedures of every financial institution.

“Our close is guaranteed 30 days after loan approval,” Young said. “Otherwise, we will pay the customer $250 toward the closing costs.The best way to start the loan process is to come into one of our branches and ask to meet with a personal banker. At that point, the borrower will be advised of the documents needed to verify income, credit, and amount of cash to close.”

In addition to stimulating the home buyer market, the low interest rates are also generating refinance activity.

But how much of a point spread between the mortgage holder’s existing interest rate and the current prevailing rate would make it worthwhile to refinance?

“We generally advise the customer that a one and a half to two point difference would certainly make it worthwhile to refinance,” Young said.”Again, we urge borrowers to come in an talk to a personal banker to discuss their individual needs and their options.

“People refinance for a variety of reasons, in addition to just lowering their monthly payment… typically debt consolidation, home improvement, a new car, school tuition. But in today’s economic climate, just creating greater liquidity by reaping the monthly savings on a lower priced mortgage is incentive enough.”

Young provided an example of a refi customer with a loan balance of $300,000 on a 30 year fixed rate mortgage loan at 6% and monthly payment obligation of $1,798.65 (principal and interest).

“By refinancing down to the current rate of 4.25% with a new 30 year mortgage, the payment would become $1,475.82… representing a savings of $322.83 a month.

“The customer might also want to consider a 15 year fixed rate mortgage at 3.75% with monthly payments of $2,181.67 covering principal and interest.The monthly payments would be higher due to the shorter amortization period, but the savings in interest over the life of the loan could be as much as $139,575.

“The best course of action is always to discuss your needs and loan options face to face with an experienced lender. In this fast-moving marketplace, my advice to anyone hoping to buy or refi is to begin the process as soon as possible. Rates this low can’t last forever and it could be a while before they come around again.”

See More Listings